Real Estate Investment: Opportunities and risks for doctors

For many medical professionals, real estate is far more than just "concrete gold" or an inflation hedge. It is a currency-independent, relatively stable, and predictable asset class, which is very well suited as a strategic building block for wealth accumulation and retirement planning .

Unlike purely monetary assets (such as call money, fixed-term deposits, or traditional life insurance policies), real estate represents tangible assets, whose development primarily depends on location, demand, and property quality, and less directly on currency fluctuations or short-term whims of the capital markets. Properly structured, real estate allows you to:

- generate ongoing, largely predictable income,

- build wealth long-term,

- and strategically utilize tax benefits.

This article is aimed at medical professionals who view real estate not merely as a "parking spot" for existing assets, but as a consciously employed instrument for professional wealth accumulation.

Advantages: Why Real Estate Can Be an Attractive Investment

Real estate has long been considered a value-retaining asset class. Especially in uncertain times, many investors specifically seek security in tangible assets like real estate. For doctors with a stable income, real estate investments offer several attractive advantages: ongoing cash flows, real assets, and tax benefits.

Stable Rental Income and Wealth Accumulation

A key argument for real estate as an investment is the ongoing rental income, which generates largely predictable, passive income. Unlike highly volatile stock prices or dividends, long-term rental agreements usually offer reliable, monthly cash flows. For medical professionals, this can be a "second pillar" alongside practice or employee salaries, increasing financial independence.

In the long term, a rented property also contributes significantly to wealth accumulation :

- In many regions of Germany, real estate prices have significantly increased over longer periods, especially in economically strong cities.

- At the same time, it holds true: "The tenant pays back the loan"- The rental income covers a large part of the loan installment.

- With each repaid installment, a larger share of the property belongs to you. Your equity grows while the bank debt decreases.

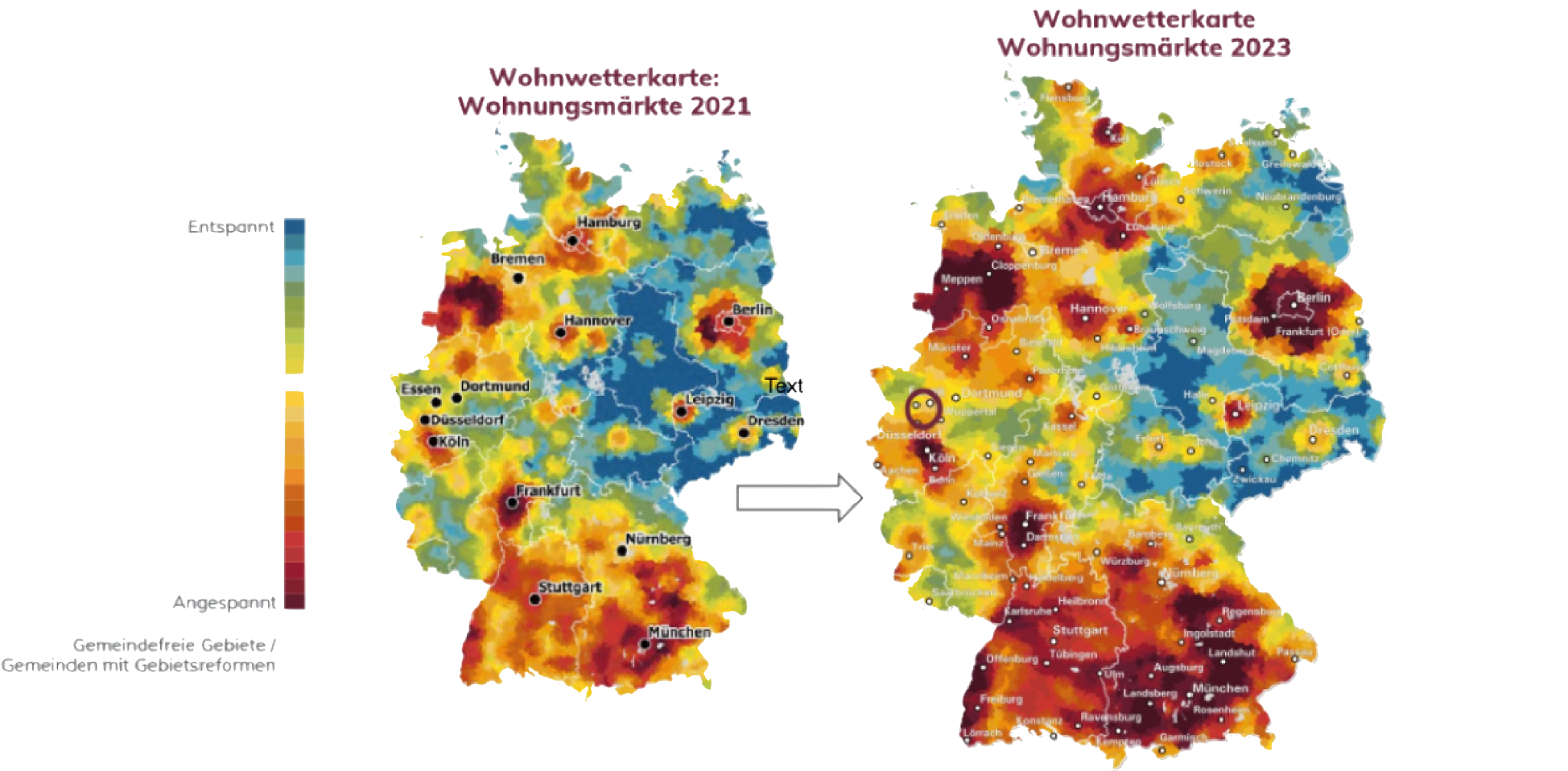

Source: Wohnwetterkarte | https://www.bpd-immobilienentwicklung.de/aktuelles/marktforschung/wohnwetterkarte/

Inflation Protection and Currency-Independent Investment

Real estate is often considered as natural inflation protection . The reason is: While monetary assets lose purchasing power during inflation, real assets usually retain their real value better or even increase in value.

When prices and living costs rise, typically so do rents and property values follow suit. Landlords can adjust rents (within legal regulations) in the medium term, and properties themselves are often valued higher in an inflationary environment over the long term.

More importantly in your context: real estate is more currency-independent than many traditional financial investments. Its value is based on:

- real scarcity of housing,

- location quality,

- and actual demand,

and not just on a promise from a bank or company. Studies and analyses by major institutions like Deutsche Bank confirm that home ownership can provide long-term good protection against loss of purchasing power can offer.

For medical professionals who don't want their hard-earned money to lose value in a savings account, this real asset characteristic is a key advantage.

Tax advantages for real estate investors (e.g., depreciation)

An extremely important advantage of real estate investment is the tax effects – especially for professions with a high marginal tax rate, such as doctors.

Key tax levers include:

- Depreciation (AfA)

- For residential properties, the building value (excluding land) can be depreciated linearly at typically 2% p.a. over 50 years.

- This applies particularly to new constructions and extensively renovated properties; for listed buildings and certain renovations, even increased or special depreciation allowances are possible.

- Interest expenses and ongoing income-related expenses

- Interest on real estate loans can be fully deducted as income-related expenses.

- Similarly, ongoing expenses – e.g., maintenance, renovations, property management, insurance – reduce the taxable income from rental and leasing.

- Strategically utilize modernization measures

- If modernizations are classified as maintenance expenses , they can often be claimed as tax-reducing expenses in the year of implementation or spread over a few years.

- This way, a significant portion of the initial investment costs can be recovered through tax declarations as early as the year following the investment.

Doctors in particular benefit here disproportionately: For most, 42 cents are reimbursed by the tax office for every euro reported as a loss in the tax balance sheet. In practice, the tax office thus covers a significant portion of your investment. Properly structured, the property therefore becomes a tax-saving model and wealth-building component.

Risks and Disadvantages of Real Estate Investment

As clear as the opportunities are, real estate is not a guaranteed success. Mistakes primarily occur when property quality, location, and financials are not properly vetted.

High Capital Investment, Incidental Costs, and Ongoing Expenses

Real estate requires a significant capital investment. In addition to the pure purchase price, the following are incurred in Germany, among others:

- Real estate transfer tax (approx. 3.5–6.5% depending on the federal state),

- Notary and land registry fees (approx. 1–2%),

- Broker's commission (if applicable).

In total, this can easily amount to 5–12% in additional incidental costs, which must be financed or paid in cash. Especially for first-time investors, experts often advise contributing at least 10-20% as equity for the investment.

In practice, problems arise if you:

- only look at the price per square meter and ignore other relevant factors

- are swayed by high, promised rents instead of demanding clear proof of existing demand

- the renovation status, the owners' association minutes, the reserves, and market rents are not seriously checked.

Especially with older properties, a "bargain" with hidden renovation backlogs can quickly become expensive. You then end up with a long-term financial commitment that feels wrong emotionally and economically.

Furthermore, real estate is illiquid. Selling takes time and money, unlike funds or ETFs, which can be quickly liquidated. Anyone who wants to remain flexible in the very short term should therefore carefully consider how much capital they want to tie up in a property.

Vacancy Risk and Property Management Effort

A property is only profitable if it is rented out and professionally managed . The vacancy risk heavily depends on the location:

- In many regions of Germany, there is still a housing shortage. There, structural vacancy at market-rate rents is rather uncommon.

- In regions with population decline or oversupply , the situation is different. Here, vacancy can become a very real and expensive risk.

Anyone who fails to assess the location, for example, based on population trends, rent indexes, and vacancy rates, significantly increases their risk.

In addition, there's the administrative burden: rental agreements, utility bill statements, coordinating tradespeople, legal issues. While problematic tenants or payment defaults are statistically rarer than headlines suggest, they can be extremely time-consuming in individual cases.

Many smaller, privately acquired properties are rented out without professional management, which can quickly become a significant burden. A good property management company costs money, but saves time, stress, and mistakes. At the same time, professional management offers the opportunity to align one's investment according to economic criteria, rather than based on the length of one's personal commute.

Those who leverage networks of professional investors or specialized consultants often gain access to verified property managerswho have already proven their quality.

Some developers even offer rental guarantees for high-quality projects if they are convinced of the low risk of the location. This saves one from needing rent default insuranceto cover risks like vacancy or rent default.

Market fluctuations and potential loss of value

Compared to stocks, real estate is considered relatively stable in value, but it is not immune to market fluctuations:

- Rising interest rates can suppress demand for purchased properties and put pressure on prices.

- Regulatory interventions (e.g., stricter rental regulations) can diminish returns.

- Local factors such as the departure of major regional employers or out-migration can make previously sought-after locations less attractive.

Depreciation is also possible, for example, if properties were bought at an inflated price just before a market correction.

The decisive factor here is the investment horizon:

- Short-term speculation ('Buy & Flip') is highly dependent on market sentiment.

- Conversely, those who opt for Buy & Hold with 10+ years are significantly less affected by short-term fluctuations – especially if cash flow, location, and property quality are right.

Strategies for Doctors as Real Estate Investors

Diversification and Setting a Realistic Investment Horizon

In the real estate context, diversification means:

- Don't invest everything in a single property

A high capital expenditure in a single property leads to a concentration risk. Several smaller units in different locations significantly reduce this risk. - Not just one type of property

In addition to traditional condominiums, for example,- care apartments,

- Listed buildings,

- shared living concepts,

- micro-apartments or student housing

may be considered.

Real estate is particularly worthwhile as a medium- and long-term investment. A time horizon of at least 10 years is realistic, also because after this period, a sale in Germany is usually tax-free.

Anyone planning for international activities or location changes in their life should definitely align their real estate strategy accordingly: the right locations, good management, a clear exit plan. This way, despite a long-term investment, one remains organizationally flexible.

Optimize financing and plan for reserves

Real estate is one of the few asset classes that allows private individuals to generate returns on borrowed capital. And here, doctors often have very good opportunities: banks consider this professional group to be very creditworthy and often offer better conditions, higher loan-to-value ratios, and sometimes even full financing including ancillary costs.

At the same time, an offer for full financing at good conditions is often an indicator that the bank itself considers the property to be solid and valuable.

Because interest on rented properties is tax-deductible, it is usually the most profitable way for investment properties to use little equity to invest and strategically use external financing to optimize returns. At the same time, the risk should not be overextended.

Key considerations:

- Moderate initial amortization (e.g., 1.5 - 2% p.a.) allows the ongoing payment to be largely covered by the rent.

- A long fixed-interest period (10–15 years) ensures a stable basis for calculations and aligns with the buy-and-hold strategy.

A practical tip based on our experience: Regional banks (Sparkassen, Volksbanken) often know their markets better than large lending institutions and frequently assess projects more realistically. It is therefore always worthwhile to compare several institutions.

It is also important: Especially for older and fully financed properties in areas with lower rental demand, adequate liquidity reserves should be factored in. While the risk of unexpected repair costs or rental defaults can largely be reduced through good planning, a certain residual risk always remains.

Seek expert advice (real estate consultants, financial advisors)

For doctors, collaborating with experienced partners when buying real estate is worthwhile. Professional advisors understand the specific needs of this professional group, save time, and provide access to vetted properties that go beyond classic portals like ImmoScout24 or ImmoWelt.

A good advisor accompanies the entire process from analysis to purchase decision and contributes vetted contacts, market knowledge, and in-depth analyses. This results in investments where defects are largely excluded and which can also be professionally managed long-term.

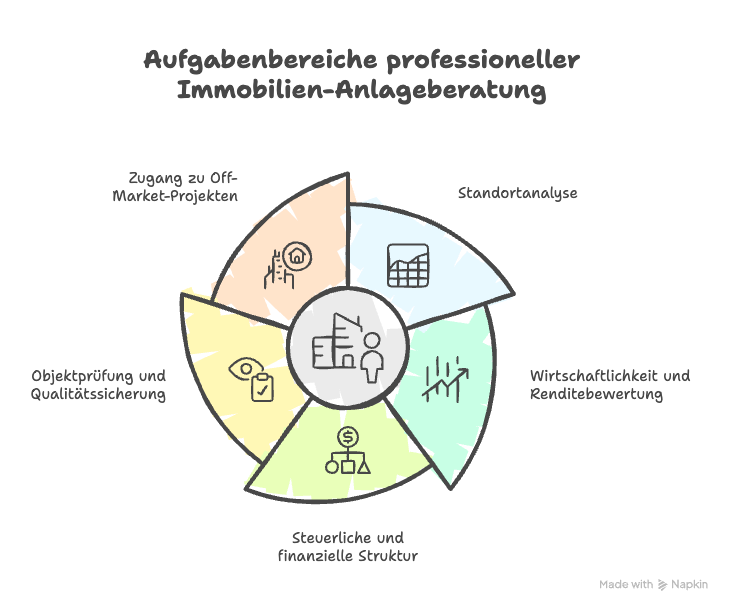

Five areas are particularly important:

- Location analysis with genuine market access

Experts use databases and tools that go far beyond public platforms. They identify trends early, assess migration, new construction activity, and rental development, and can evaluate opportunities and risks significantly better. - Profitability and Return Evaluation

Each property is evaluated based on its yield, cash flow, and multi-year projections. This quickly reveals whether it aligns with personal goals, such as wealth accumulation, retirement planning, or tax optimization. - Tax and Financial Structure

A solid strategy considers tax effects such as depreciation (AfA), special depreciation, or the deductibility of interest and modernization costs. Coordination with a tax advisor ensures a long-term sustainable financing structure. - Property Due Diligence and Quality Assurance

Pre-selected properties are offered through vetted networks and long-standing relationships. Independent experts also assess the building structure, energy efficiency, and potential risks. - Access to Off-Market and Vetted Projects

Through established partner networks, investors gain access to vetted and often unlisted properties. These off-market deals arise from close relationships with project developers, property managers, and banks, often offering better terms.

A good property is no accident, but the result of a clear strategy and professional preparation.

Source: Graphic created with Napkin.ai

Conclusion: Who benefits from real estate as an investment?

Is real estate a worthwhile investment for doctors?

In many cases: Yes, if it is professionally planned and structured.

A carefully selected, wisely financed, and tax-optimized property can:

- a strong wealth and retirement planning component be,

- create relatively stable, currency-independent values,

- Reduce taxes and deliver a solid cash flow.

It gets risky when:

- purchases are made based solely on 'gut feeling' or a property listing, without any analysis,

- quality and location factors are ignored,

- financing is over-leveraged and without a buffer,

- or professional help is completely foregone.

Doctors, in particular, have many ideal prerequisites: a stable and good income, good access to bank financing, and high predictability in their professional lives. Anyone who also brings a time horizon of at least ten years and is willing to seek support, has excellent opportunities to build lasting wealth.

Properly structured, real estate does not become a stress factor, but rather an extremely stable, currency-independent cornerstone of a private portfolio. Crucial for this are a clear strategy, professional property due diligence, and structured implementation – this is precisely where our Real Estate Investment for Doctors comes in.

- weitere Artikel

Get to know us personally

At Wealth Doctors, we understand the demanding reality you face: clinic routine, responsibility, and limited time. Our clients particularly value that we speak plainly, not just sell. And that our advice helps them make measurably better decisions. If you want that too, let's talk.