Private health insurance for resident physicians: Is joining really worth it?

The decision between statutory health insurance (GKV) and private health insurance (PKV) is a crucial step for junior doctors at the start of their career. Understanding the differences between both systems helps them better assess whether opting for private health insurance is truly worthwhile for young doctors.

The Choice Between GKV and PKV

Starting a medical career brings new responsibilities, experiences, and important decisions. One of these is the choice of health insurance. Many young medical professionals are covered by statutory health insurance during their studies. However, with the first salary increase, the question arises: Private or statutory health insurance – which is a better fit?

Junior doctors, in particular, often face uncertainty. Private health insurance offers better benefits, more customized plans, and potentially lower contributions. At the same time, critics warn of rising costs in old age, issues with benefit coverage, and the difficult return to statutory health insurance.

This article provides an overview of the prerequisites, opportunities, and risks, aiming to offer young doctors a well-informed basis for decision-making.

Prerequisites: When can junior doctors switch to private health insurance?

A switch to private health insurance is only possible if certain criteria are met. The most important criterion is the compulsory insurance threshold.

Annual Income Threshold

To switch from statutory health insurance (GKV) to private health insurance (PKV), your income must exceed the annual income threshold (JAEG). This will be in 2026 77,400 Euros gross. As the starting salary during specialist training is typically lower, most residents initially only have statutory health insurance.

Impact of on-call duties

When assessing, the actual, regular gross annual income is always decisive, not just the basic salary. Surcharges for night shifts, weekend shifts, or on-call duties can ensure that the threshold is reached earlier.

Role of the HR department

If the JAEG has been exceeded for an entire year, the HR department reports this to the individual's statutory health insurance. In doing so, it considers all regularly paid income, which for a doctor with regular duties includes not only the basic salary but also surcharges and special payments. The statutory health insurance then sends an information letter to the policyholder, informing them about the status change from a compulsory insured to a voluntary member.

Advantages of private health insurance for residents

The decision for private health insurance (PKV) is not just a matter of contributions. Especially during specialist training, it offers tangible benefits, both short-term and long-term.

Professional benefits

Insurance companies offer doctors special medical professional rates, which are more affordable and offer better benefits than standard rates. These are tailored for the training period: low contributions with high protection. Many insurers also allow a change of tariff without a new health check, for example, after passing the specialist examination.

Doctors are considered attractive customers by insurers. They are usually health-conscious, have a stable income, and use expensive services less frequently. This leads to better conditions and discounts.

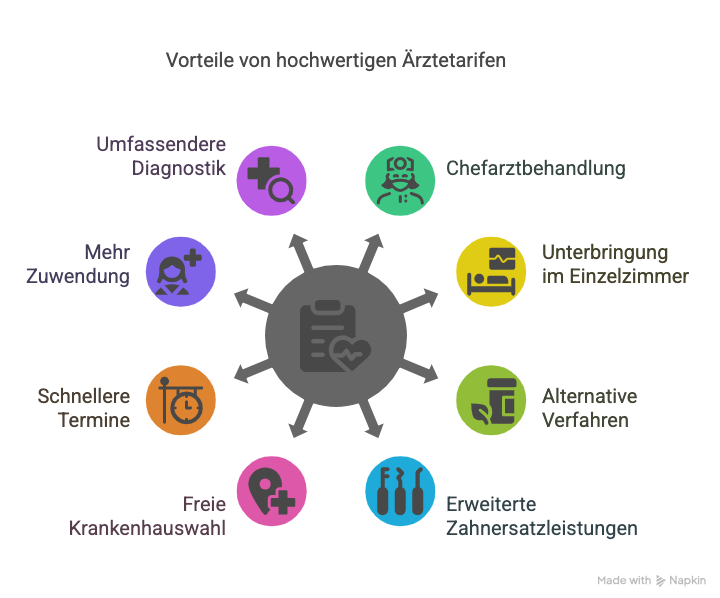

Scope of services

Private health insurance offers customizable coverage. Key features of premium medical professional plans include:

- Treatment by a chief physician or private doctor in the hospital

- Single room accommodation

- Coverage of alternative therapies

- Enhanced dental prosthetics benefits

- Free choice of hospital

In addition, private patients often receive faster appointments and more intensive care at the practice.

Graphic: Benefits of premium medical professional plans

Source: Graphic created with napkin.ai

Financial Benefits

- Premium amount: Premiums are not based on income. Even with salary increases, the private health insurance premium remains constant, provided no rate adjustments are made.

- Employer contribution: As with statutory health insurance, the employer covers half of the premium up to the maximum contribution.

- Premium refund: Those who do not submit claims often receive several months' premiums back.

- Age reserves: A portion of the premium is saved for the future to mitigate rising costs in old age.

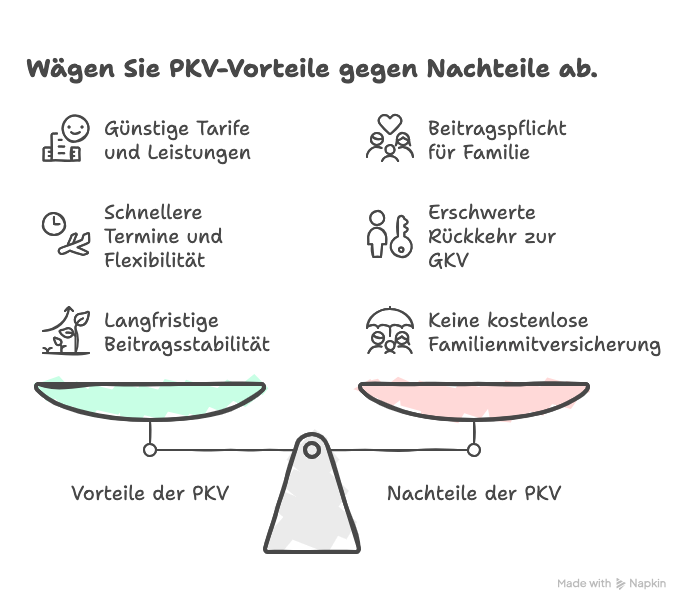

Disadvantages and Risks: When public health insurance (GKV) might be the better choice

As attractive as the benefits may seem, there are also limitations that should be considered.

Premiums in Retirement

The concern about rising private health insurance (PKV) premiums in retirement is widespread. While costs do increase with age, age-related provisions mitigate this development. Doctors in a professional pension scheme also do not have access to the health insurance for retirees (KVdR). In many cases, PKV can even be more affordable in old age.

Family Coverage

In private health insurance (PKV), spouses and children are not automatically covered. A separate premium is due for each family member. However, employers also contribute to the costs for children. Additionally, there are special, cost-effective child plans. In practice, private health insurance for a doctor with 2-3 children is usually the more profitable option if it was taken out at a young age. If both parents can be privately insured, PKV is also attractive for large families.

Return to Public Health Insurance (GKV)

A later return to public health insurance (GKV) is only possible under certain conditions, such as part-time employment below the income threshold, unemployment, or stays abroad. After the age of 55, a switch is generally not possible. Anyone who will only be temporarily subject to compulsory public health insurance again can keep their options open with a reinstatement option insurance to continue their private health insurance (PKV) contract at a later date.

Health Check

Before being admitted to private health insurance (PKV), a health check takes place. Pre-existing conditions can lead to surcharges, exclusions, or rejection of the application. For young and healthy doctors, this usually poses no obstacle.

Solidarity Principle

Public health insurance (GKV) operates on the solidarity principle: Everyone contributes regardless of risk. For some, this social aspect plays an important role.

Graphic: Advantages and Disadvantages of Private Health Insurance (PKV) for Doctors

Source: Self-created with Napkin.ai

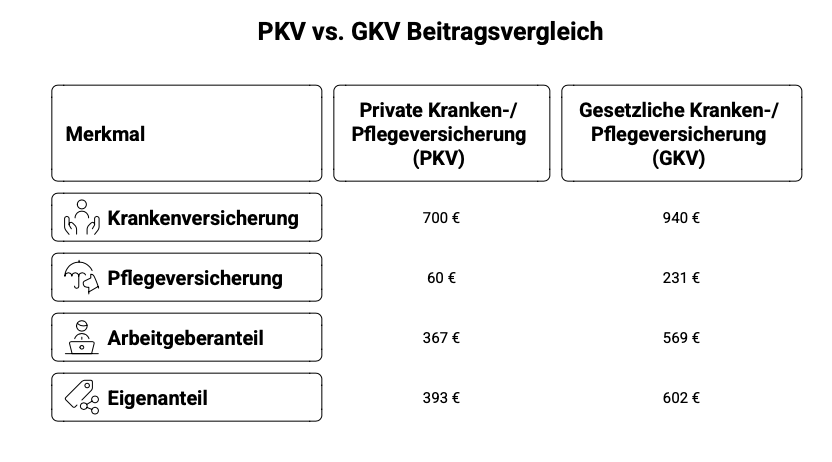

Costs of private health insurance for resident physicians

The costs of private health insurance for resident physicians play a crucial role in the decision between public and private health insurance.

Example Calculation

A resident physician pays approximately 760 Euros per month for health and long-term care insurance. With the employer's contribution, the out-of-pocket share is reduced to approximately 393 Euros. For comparison: The maximum contribution in the public system in 2025 is approximately 1171 Euros, with the out-of-pocket share being 602 Euros. This means the monthly pre-tax savings can be over 200 Euros.

Graphic: Private vs. Public Health Insurance Contribution Comparison

Source: Self-created with Napkin.ai

Premium Structure

The premium amount depends on the entry age, health status, and scope of benefits. Age-related provisions ensure that premiums remain stable during retirement.

Additional options such as deductibles or premium relief tariffs allow for further adjustments.

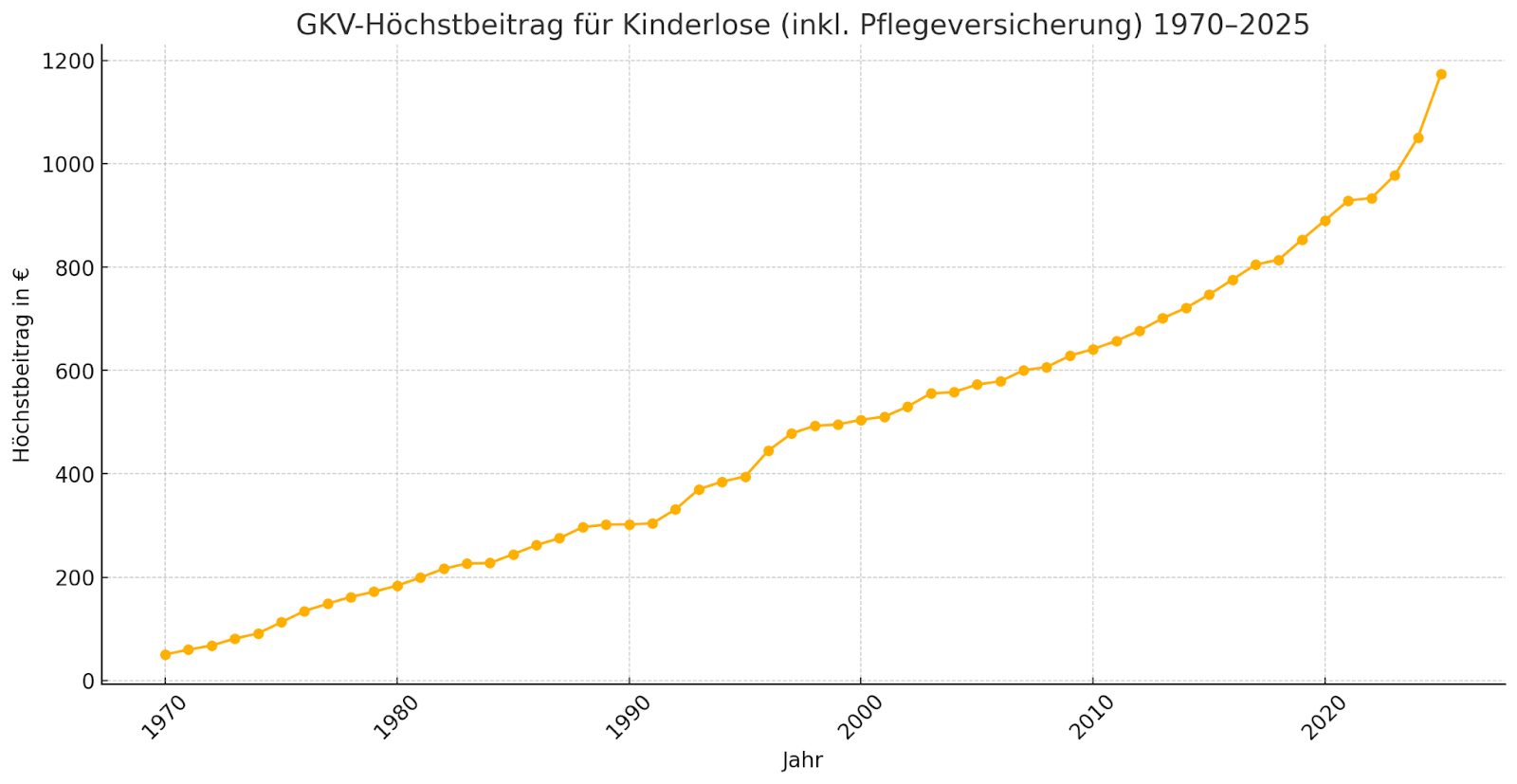

Dynamics: Premium Development of Private and Statutory Health Insurance

Premiums in the Statutory Health Insurance (GKV) automatically increase with income. The income threshold, above which the maximum contribution had to be paid, was €66,150 gross annual income in 2025. Higher earners thus bear the largest share of general premium increases for healthcare costs within the social system.

Chart: Development of the Maximum Contribution in Statutory Health and Long-Term Care Insurance (1970-2025)

Source: Self-created with ChatGPT

In the Private Health Insurance (PKV) however, premiums are independent of income. Premiums develop proportionally to healthcare costs and depending on the scope of coverage. Studies show that premium increases for most private health insurers are significantly lower than those in statutory insurance.

Important for Doctors: Pensioners from professional pension schemes (Versorgungswerke) are not entitled to health insurance for pensioners. Therefore, doctors insured under the statutory system pay the full contribution rate for health and long-term care insurance (19.6%) on their pension and private income during retirement. With a good premium relief tariff, private health insurance is almost always the significantly more affordable option in the long run.

Additional Options and Deductible

With private health insurance, you can actively shape your premium. For example, those who choose a deductible of, for example, €500 or €1,000 annually, will pay a correspondingly lower monthly premium. At the same time, many insurers offer attractive bonus programs and refunds for not claiming benefits.

Furthermore, premium relief plans help to further mitigate costs in retirement.

This flexibility offers a degree of freedom that is not available in statutory health insurance.

Conclusion: Private Health Insurance for Junior Doctors, an Individual Decision

Private health insurance offers many clear advantages: better benefits, flexible plan options, and financial relief in the first years of your career.

However, it's important to note: options for returning to statutory health insurance are limited, premiums can rise in retirement, and families require individual coverage. There is no one-size-fits-all recommendation. Every junior doctor should make the decision based on their personal situation.

How Wealth Doctors Supports Young Doctors

A decision for or against private health insurance should not be made without expert knowledge. Our consultation, specifically developed for medical professionals, Private Health Insurance Consultation takes into account your individual life and income situation – from choosing the right tariff and realistically assessing premium development to strategic future planning.

- weitere Artikel

Get to know us personally

At Wealth Doctors, we understand the demanding reality you face: clinic routine, responsibility, and limited time. Our clients particularly value that we speak plainly, not just sell. And that our advice helps them make measurably better decisions. If you want that too, let's talk.