Occupational disability for doctors: understand it properly and secure optimal protection

The Occupational Disability Insurance for Physicians (BU) is one of the most important forms of protection in a medical career. It protects physicians from the financial consequences if they can no longer practice their profession, either fully or partially. Especially for young physicians, the question arises early on whether coverage through their professional pension scheme alone is sufficient. In this article, you will learn the differences, why early enrollment makes sense, and how to find the right policy.

Why Occupational Disability Insurance can be Crucial for Physicians

Even though physicians are covered by their professional pension scheme, this protection is often insufficient. Benefits usually only kick in with full occupational disability, meaning when no medical activity is possible anymore. In reality, this is only the case in rare exceptions.

Private Occupational Disability Insurance (BU) , on the other hand, pays out even with 50 percent occupational disability and focuses on the last profession practiced. Whether a BU is worthwhile depends on income, ongoing commitments, loans, and long-term life planning.

Differences Between Professional Pension Scheme and Private Occupational Disability Insurance (BU)

The BU pension from the professional pension scheme is only paid when a full occupational disability is present. This means that physicians can no longer fully perform their medical activities. A surgeon who can no longer operate but could still write expert opinions or work in teaching receives no benefits.

The private Occupational Disability Insurance (BU) kicks in significantly earlier. Even with a 50 percent impairment, the agreed-upon pension is paid. Good policies also waive so-called reassignment clauses, which could otherwise refer you to another profession or areas of activity within your own profession. This way, you are financially protected if you can no longer perform your specific medical activities.

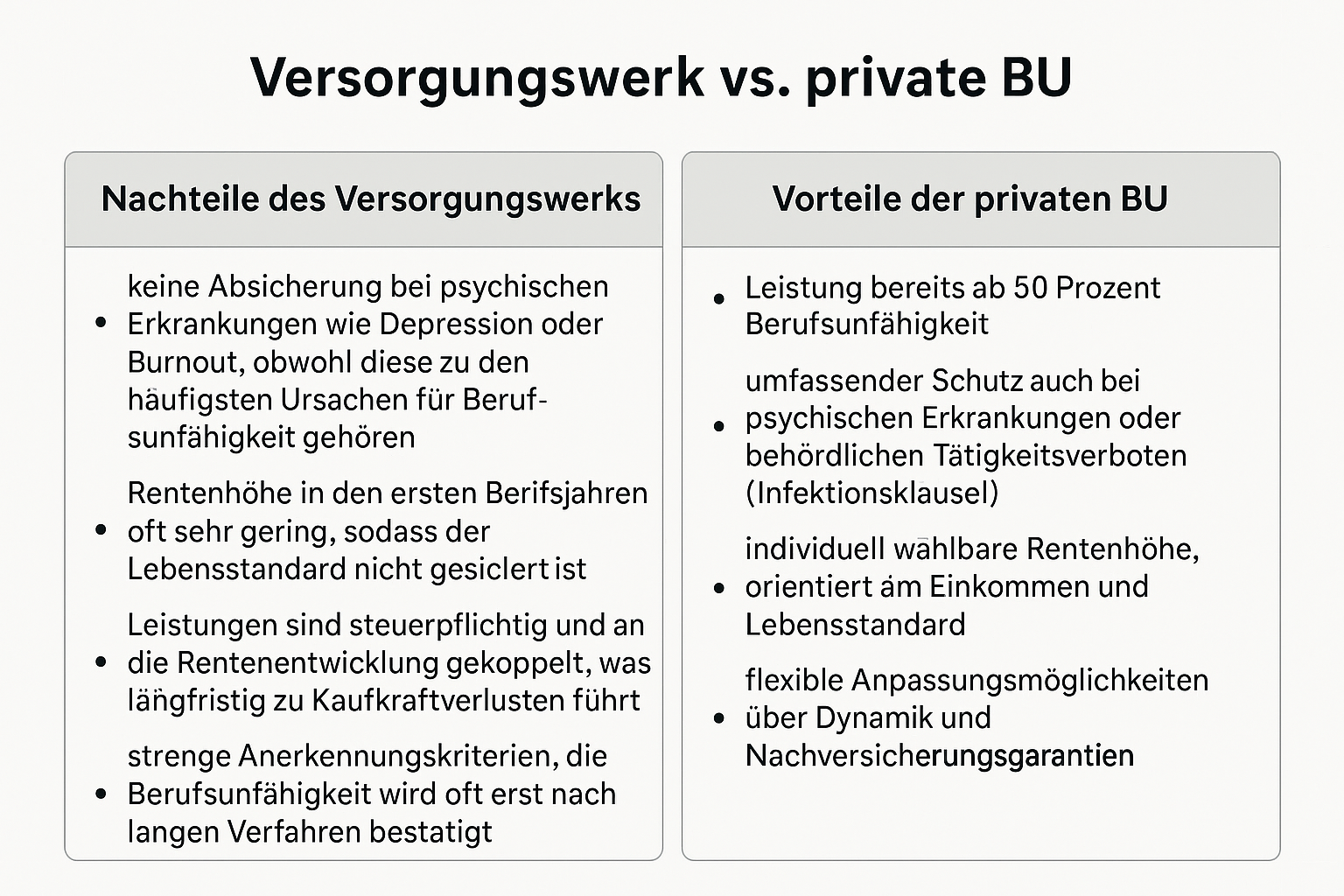

Disadvantages of the Professional Pension Scheme at a Glance

- No coverage for mental illnesses like depression or burnout, even though these are among the most common causes of occupational disability

- Pension amount often very low in the early years of employment, making it difficult to maintain one's standard of living

- Benefits are taxable and linked to pension trends, leading to a long-term loss of purchasing power

- Strict eligibility criteria; occupational disability is often only confirmed after lengthy procedures

Advantages of Private Occupational Disability Insurance

- Benefits payable from 50 percent occupational disability

- Comprehensive coverage, including for mental illnesses or official prohibitions on activity (infection clause)

- Individually adjustable pension amount, based on income and standard of living

- Flexible adjustment options through dynamic clauses and guaranteed increases

Occupational Disability Insurance at Different Career Stages

The demands and risks in the medical profession change significantly depending on the career stage. Accordingly, occupational disability insurance for doctors should be adapted. From medical school to a chief physician position, it's worthwhile to plan for appropriate protection early on.

Medical School

Taking out occupational disability insurance early offers clear advantages that medical students often underestimate:

- Affordable premiums thanks to student rates

- Simple and usually straightforward health assessment

- Option to secure a disability insurance pension of up to 2,000 Euros

- Guaranteed increase option for future salary increases without a new health examination

It's particularly beneficial for students to start early, as pre-existing conditions are still rarely an issue and insurers offer attractive entry conditions. Anyone who takes out disability insurance during medical school secures the best conditions for low premiums and maximum flexibility.

Specialist training period

During specialist training, the demands increase significantly: shift work, high time pressure, constant responsibility, and increasing psychological stress. Studies show that young doctors, in particular, have an increased risk of burnout or stress-related illnesses.

A disability insurance for resident doctors protects not only income during this phase, but also the painstakingly built-up standard of living. Anyone starting a family, financing a house, or taking out loans to set up a practice is existentially at risk without disability insurance.

A key advantage: Those who secure coverage early still benefit from low premiums and simple acceptance conditions. Pre-existing conditions can later lead to risk surcharges or even rejection. However, when choosing the right insurance, potential career paths should definitely be taken into account.

Specialist, Senior Physician, Chief Physician

With growing professional experience and increasing income, the demands on coverage also rise. As a guideline, the disability insurance pension should be at 75 to 80 percent of net income to cover ongoing costs.

Thanks to guaranteed increase options, doctors can adjust their disability insurance pension in the event of salary increases, practice establishment, marriage, or the birth of a child, without a new health examination. This ensures that coverage always remains up-to-date and flexible.

For self-employed or established doctors, it is particularly important to secure not only their own standard of living, but also fixed practice costs to cover. These include rent, leasing rates for equipment, or personnel costs. Policies with reorganization clauses and with concrete reassignment are crucial here to best secure individual medical practice.

What Doctors Should Look For When Choosing a Policy

Not all occupational disability insurance policies for doctors are created equal. The differences often lie in the contract details. These specific points determine whether you are truly covered or if there are gaps in an emergency. Therefore, you should pay particular attention to the following criteria:

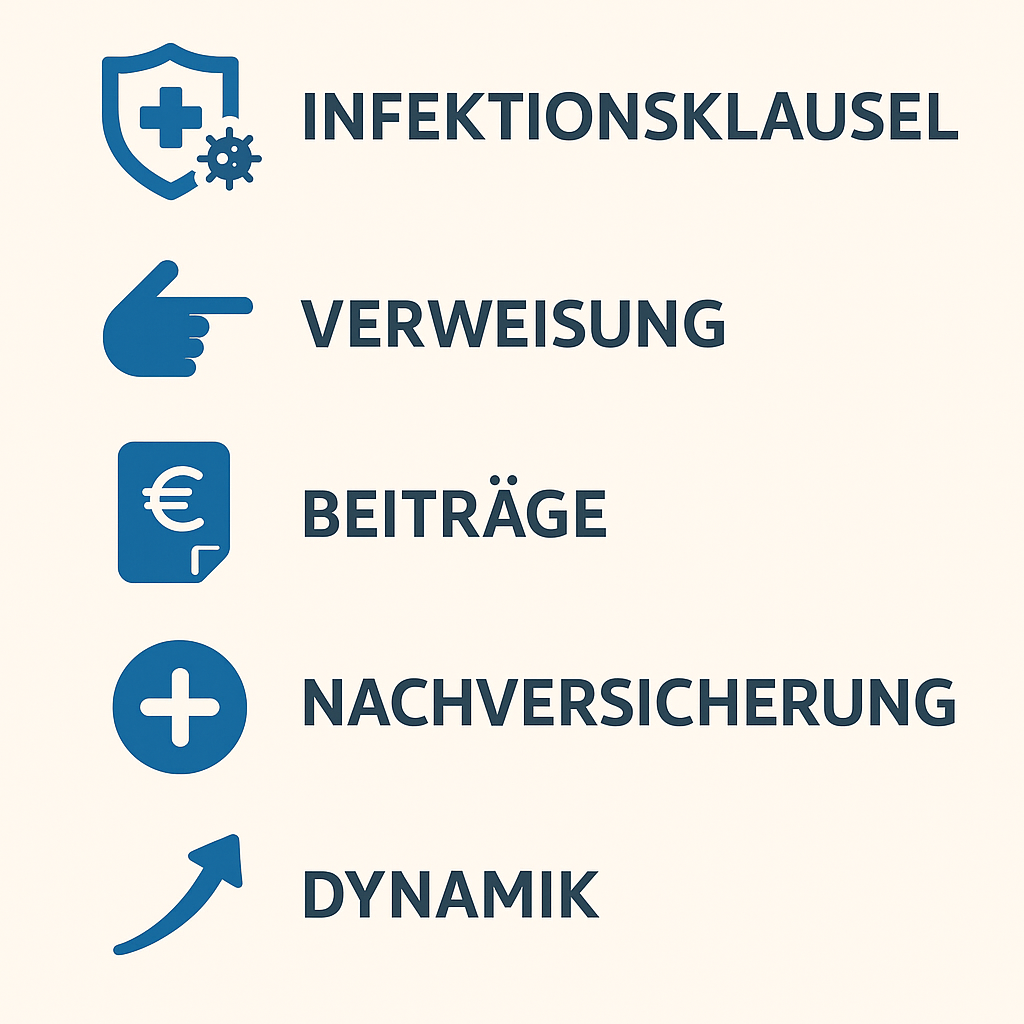

Infection Clause

For doctors, the Infection Clause is of central importance. It applies when an official ban on activity is issued, for example, due to the risk of infection. Even if you are physically healthy, you would no longer be able to practice your medical profession in such a case. With an infection clause, you receive benefits; without it, your protection would be incomplete in such situations.

Reassignment Clause

Almost all occupational disability policies waive the abstract reassignment. This means you don't have to accept another profession just because you are theoretically capable of doing so. With the concrete reassignment the insurer can stop benefits if you are already actually working in a comparable activity, such as an expert or consultant. For surgeons in particular, waiving the concrete reassignment clause is especially important, as this is the only way to truly protect their core activity.

Premium Information

Pay attention to how large the difference between gross premium and net premium is.

- The gross premium is the maximum premium and is guaranteed.

- The net premium is the actual premium to be paid, reduced by the insurer's surpluses.

If the profit participation decreases, the net premium can increase. With high-quality companies, this difference is a maximum of 35%. If there is a large gap between the two premiums, the risk of experiencing significant premium increases in the future rises.

Guaranteed increase option

The guaranteed increase option is particularly important for doctors. It allows you to increase your disability insurance benefit in the event of life changes such as marriage, birth of a child, salary increase, or starting a practice, without a new health check. This keeps your coverage flexible and allows it to grow with your career.

Automatic adjustment

The automatic adjustment ensures that the benefit amount and premiums automatically adjust each year. This keeps your disability insurance stable against inflation and rising income. An annual adjustment of between two and five percent is recommended. Without this adjustment, the purchasing power of your disability insurance benefit decreases over the years.

Many companies offer the option to suspend the automatic adjustment without losing the right to future increases.

Graphic: Checklist "The five most important criteria for doctor-specific tariffs" with suitable icons for infection protection, abstract referral clause, premiums, guaranteed increase option, and automatic adjustment.

Is combining with a pension plan advisable?

Some insurers offer the option to combine occupational disability insurance directly with a pension plan. This is possible either as a Flex or a so-called Rürup pension with an additional occupational disability component. At first glance, this solution can seem attractive because both important issues – protecting your earning capacity and building up your retirement pension – are combined in one contract.

Advantages of a Combination Solution

A combination contract offers several advantages. If occupational disability never occurs, it ensures that funds from the contract are still paid out. Furthermore, with a Rürup pension, contributions for the occupational disability insurance can be tax-deductible, which reduces the monthly cost. In addition, in the event of occupational disability, the insurer takes over the contributions for the pension plan. This means that even with a prolonged illness or an occupational ban, the pension plan continues.

Disadvantages of a Combination Solution

However, the disadvantages should not be underestimated. Combination contracts are less flexible because they link both types of coverage. Anyone who cancels or pauses the contract typically loses both the occupational disability insurance coverage and the pension plan component. Furthermore, the choice of providers is limited. The best occupational disability insurer is not automatically the best provider for pension plans. Another disadvantage: the occupational disability pension from a Rürup pension is usually fully taxable.

[SEG 9]

Alternative: Two-Contract Solution

A popular alternative is the two-contract solution. Here, a standalone occupational disability insurance policy is taken out, and the pension plan is set up either separately or with an additional occupational disability component. This option offers more flexibility, as both contracts can be designed, adjusted, or cancelled independently. When structured correctly, this can at least allow occupational disability contributions to be partially tax-deductible, while avoiding the disadvantages of subsequent taxation of the occupational disability pension. The contract durations can also be planned separately, which creates additional freedom.

Occupational Disability Consulting with the Wealth Doctors

Solid occupational disability protection requires more than just comparing rates. The Wealth Doctors guide doctors step-by-step:

Analysis of personal situation and financial obligations

- Assessment of coverage needs

- Anonymous preliminary risk inquiries with insurers

- Comparison of rates specifically for doctors

- Support with application and follow-up

- Ongoing support for changes such as salary increases or starting a family

You can find more information on our page about occupational disability insurance for doctors. There you'll find all the details and can directly request a no-obligation consultation.

- weitere Artikel

Get to know us personally

At Wealth Doctors, we understand the demanding reality you face: clinic routine, responsibility, and limited time. Our clients particularly value that we speak plainly, not just sell. And that our advice helps them make measurably better decisions. If you want that too, let's talk.