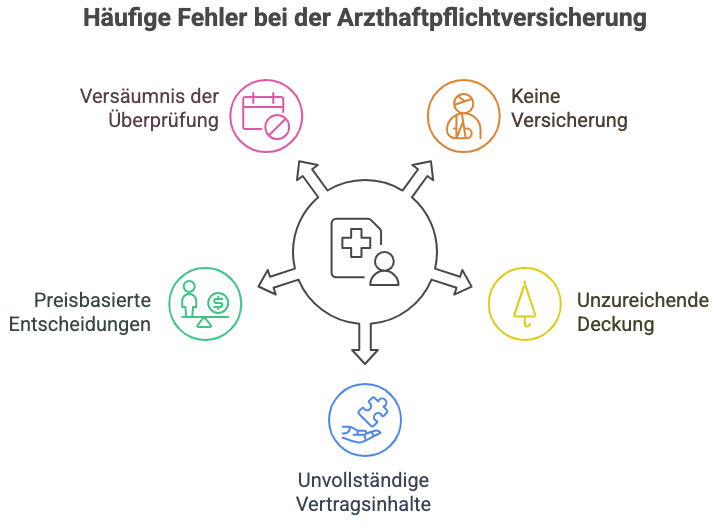

The 5 most common mistakes in medical malpractice insurance and how doctors can avoid them

As a doctor, you bear enormous responsibility. Even a small mistake can have major consequences. This makes reliable professional liability insurance for doctors, also known as medical malpractice insurance, all the more important. It protects against financial risks arising from treatment errors, failures to inform, or missing documentation.

But a policy alone is not enough. Many medical professionals overlook common pitfalls when taking out or maintaining their insurance. Every doctor has different requirements, depending on their specialty, scope of activity, and risk profile. In an emergency, inadequate coverage can prove costly. In this article, you will learn about the five most common mistakes and how to avoid them.

Source: Self-created with Napkin.ai

Graphic: Illustration "The five most common mistakes in medical malpractice insurance"

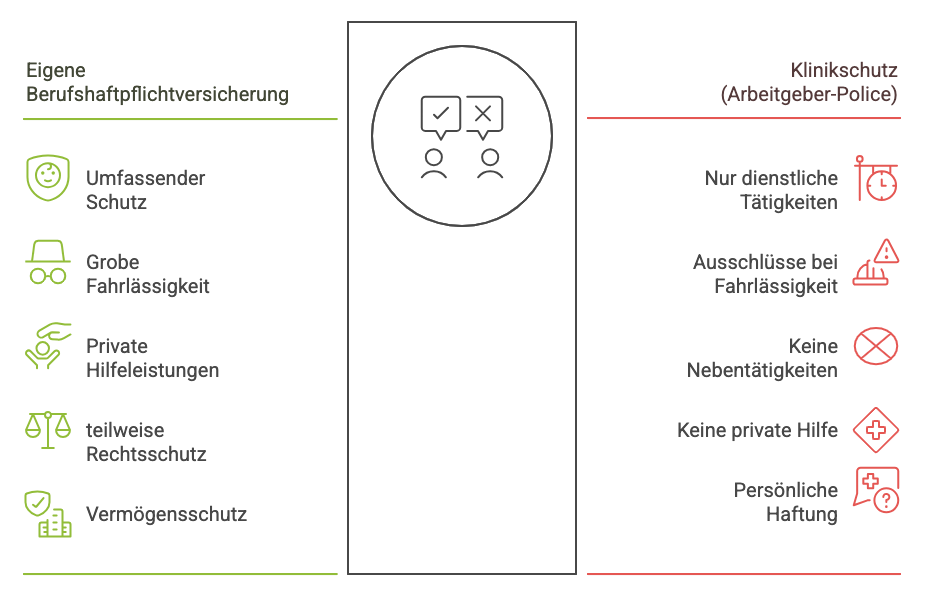

Mistake 1: Not taking out your own professional liability insurance

Especially at the beginning of their careers, many doctors rely on the protection provided by the hospital. However, this protection is usually insufficient. Hardly any hospital policy fully covers risks such as gross negligence, secondary activities, or allegations of insufficient informed consent.

Since doctors in Germany are always personally and unlimitedly liable, without your own professional liability insurance, you risk your private assets and, in the worst case, your entire livelihood.

Is medical malpractice insurance legally required?

There is no direct obligation in Germany, unlike in many other countries. However, § 21 of the Federal Medical Practitioners' Act requires adequate coverage. Gross negligence or private assignments, in particular, are usually not covered by the employer.

Tip: Whether during your studies, specialist training, or as a specialist, your own medical malpractice insurance is indispensable. For young doctors, there are affordable rates, sometimes even premium-free offers through professional associations.

Source: Self-created with Napkin.ai

Graphic: Icon graphic "Hospital protection vs. own policy"

Mistake 2: Choosing an insufficient sum insured

Many older policies only cover two or three million euros. That is too little today. Even if pain and suffering compensation is limited, high costs arise from loss of earnings and lifelong care.

Example: An internist overlooks a bacterial infection in a lab report. The patient develops sepsis and remains in need of care. Care costs of 25,000 Euros per month accumulate to millions over years. If the sum insured is set too low, you pay the rest yourself.

How high should the sum insured be?

A minimum of five million Euros per claim is recommended. Even better is coverage of up to ten million Euros. Also, ensure that it is genuine per-claim coverage and not an annual maximum.

Tip: Increase your sum insured as soon as you implement new procedures or your responsibilities grow, for example, when establishing a practice or specializing.

Mistake 3: Gaps in coverage due to incomplete contract terms

Many doctors believe that one policy covers everything. However, dangerous gaps often remain, which can become costly in the event of a claim.

Typical examples of coverage gaps:

- New assistants are hired but not reported to the insurance company.

- A change to another specialty, such as aesthetic medicine, occurs without adjusting the contract.

- Ancillary activities as an emergency physician or expert witness are not covered because they were not declared.

What should you look out for?

- Coverage for treatment, informed consent, and documentation errors

- Coverage for personal injury, property damage, and financial losses

- Co-insurance for practice staff, medical interns (Famulanten), and practical year (PJ) students

- Inclusion of unlimited post-liability

- Extended criminal legal protection for attorney and court fees

Tip: Inform your insurance company immediately of any changes. If it's not reported, it won't be covered in an emergency.

´

Source: Self-created with napkin.ai

Graphic: Checklist 'Key Contractual Provisions of Medical Malpractice Insurance'.

Mistake 4: Deciding solely based on price

Especially during your residency, price is a significant factor. However, a cheap plan is useless if crucial benefits are missing when you need them most. Budget plans often cut corners on important areas like criminal legal protection or coverage for new procedures.

Not every provider with 'Doctors' in its name automatically offers the best protection. The decisive factors are the contract terms and the quality of service in the event of a claim.

How do you find the right provider?

- Compare price and benefits, not just the premium amount.

- Consider the specific requirements of your specialty.

- Verify that post-liability, coverage for modern procedures, and a strong reputation for handling claims are guaranteed.

Tip: Seek independent advice. A broker specializing in medical professionals can help you find the best combination of price and benefits.

Source: Self-created with Napkin.ai

Graphic: Comparison graphic "Budget plan vs. high-quality plan"

Mistake 5: Not regularly reviewing your contract

Many doctors take out their medical professional liability insurance once and then don't give it another thought. However, the profession and the market are constantly changing. New procedures, increasing risks, and better plans make regular review essential.

How often should you review your policy?

Ideally every two to three years, or whenever something changes in your professional life. This includes starting a practice, achieving specialist status, or moving abroad.

Conduct in the event of a claim

If a claim arises, inform your insurer immediately. Do not make any payments out of pocket or admit fault before consulting with your insurer.

Tip: An experienced advisor will support you not only when taking out the policy, but also in the event of a claim.

Conclusion: How to avoid common mistakes

Professional liability insurance is essential for every doctor. Here are the five most important points:

- Have your own policy and don't rely on your employer's.

- Choose a sufficiently high sum insured of at least five million Euros.

- Regularly review your contract and report any changes.

- Focus on the scope of services, not just the price.

- Benefit from independent advice to find the right plans for you.

What Wealth Doctors can do for you

As independent brokers for medical professionals, Wealth Doctors will support you long-term.

Our services at a glance:

- Management of your medical malpractice insurance

- Adjustments for new activities or changes

- Support in the event of a claim, including communication with the insurer

- Regular review of your insurance coverage with suggestions for optimization

This ensures you are comprehensively protected and don't have to struggle through complicated contract terms yourself. If you want to review or optimize your medical malpractice insurance, schedule a non-binding consultation with Wealth Doctors. Together, we will find the right protection for your individual situation.

- weitere Artikel

.jpeg)

Get to know us personally

At Wealth Doctors, we understand the demanding reality you face: clinic routine, responsibility, and limited time. Our clients particularly value that we speak plainly, not just sell. And that our advice helps them make measurably better decisions. If you want that too, let's talk.