US life settlements: The perfect investment for physicians?

As their careers progress, many doctors want not only to invest their assets profitably but, above all, to secure them in a value-stable manner. Between hospital routines and practice operations, there's little time to delve deeply into time-consuming investment forms like real estate or active stock management. This leads many doctors to ask: Is there an investment vehicle where they can indirectly use their own medical expertise as a basis for valuation, which simultaneously protects capital and invests independently of traditional market movements? US secondary market policies, or life settlements, could be precisely the alternative investment vehicle that offers stable returns with low volatility.

This guide explains what these "used" life insurance policies are all about, how they work, what advantages and risks they entail, and how doctors, in particular, can benefit from them. We also show how Wealth Doctors assists with investments in US secondary market policies and what to look out for.

What Are US Secondary Market Policies?

US secondary market policies are existing life insurance policies from the USA that are sold by their original owner to investors. For investors, they primarily represent a strategic addition to existing investments such as stocks, real estate, or funds, as they introduce an additional, largely market-independent source of income into the portfolio. Instead of simply canceling a policy and receiving only the low surrender value from the insurance company, the policyholder in the USA can sell their policy on the secondary market to a third party, thereby enabling investors another form of diversification and asset protection.

The investor then takes over the premium payments and, in return, receives the agreed-upon death benefit upon the death of the insured person.

This concept has been practiced in the USA since a landmark Supreme Court ruling in 1911 (Grigsby vs. Russell case) and has created an established market. In Germany, however, there is no comparable broad secondary market for life insurance policies, as these have a fixed term and therefore do not guarantee a payout if the person lives longer.

US secondary market policies are therefore also used by European investors to benefit from the regulated practice in the USA of utilizing life insurance policies on the secondary market. They are often referred to as "used" life insurance policies or, in industry jargon, as life settlements.

A typical US secondary market policy, for example, is a whole life insurance policy of an older or seriously ill US citizen (often 70+ years old) who no longer needs the insurance or no longer wishes to pay the premiums. Often, specific reasons lie behind the desire to sell, such as high hospital and treatment costs or the wish to fulfill a last dream and consciously shape their remaining lifetime. By selling the policy, the policyholder receives immediate liquidity, which makes these plans possible.

A specialized company determines the value of the policy based on the insured person's remaining life expectancy, the sum insured, and the expected premiums.

The investor buys the policy for an amount that is higher than the surrender value but significantly lower than the actual insurance benefit. Both sides benefit: The seller immediately receives an attractive sum in cash and gains financial flexibility, while the buyer (investor) can expect a predictable return when the policy eventually pays out.

How Does the Secondary Market for Life Insurance Work?

The secondary market process can be outlined in a simplified form as follows:

A policyholder in the USA, usually elderly or seriously ill, sells their life insurance policy through a licensed life settlement provider. This provider examines the policy and the insured person (including health data) and brokers the sale to investors. These investors select policies based on the complete health data provided by the sellers.

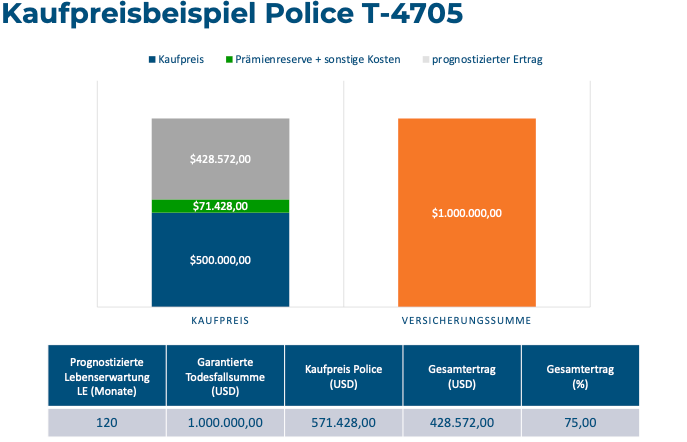

Practical Example:

A seriously ill 58-year-old policyholder sells their term life insurance policy worth 1,000,000 USD on the secondary market for 500,000 USD and receives immediate liquidity.

The buyer takes over the premium payments and, in the event of a claim, receives the guaranteed sum insured of 1,000,000 USD. The return is derived from the difference between the purchase price, ongoing costs, and the eventual payout.

As a German investor, you do not invest directly in the USA. Instead, investments are typically made through a special trust or account structure.

At its core, investing in US secondary market life insurance policies means becoming the beneficial owner of one or more US life insurance policies, including all rights to the death benefits.

Important to know: The acquired policies typically belong to large, financially strong US insurance companies, such as MetLife, Prudential, or New York Life. These companies have first-class credit ratings (A+ or even A++ from rating agency A.M. Best). The payout of the insured amount can therefore be considered guaranteed.

At the same time, the US life insurance market is strictly regulated. In most US states, there are clear legal requirements for life settlements that protect both sellers and buyers. The combination of high creditworthiness of the insurers and regulation ensures that investors can rely on the contractually guaranteed payouts.

Since 1911, a professional, highly regulated, and very liquid market has developed in the USA. Today, policies worth several billion US dollars are traded annually.

On the buyer side, there are also many large institutional investors such as pension funds, insurance companies, reinsurers, family offices, and specialized investment firms. These investors use life settlements as a stable and predictable investment component with low correlation to traditional capital markets. In some cases, they are even held in general accounts or strategic value preservation reserves, as the payouts are clearly defined and structurally predictable.

(Note: In Germany, profits from life settlement investments are generally taxed for private investors like other capital investments with the flat-rate withholding tax (25% plus solidarity surcharge/church tax). Details can be found in the FAQ section.)

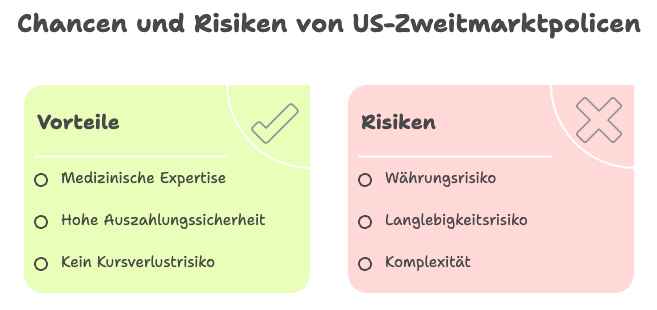

What advantages do US secondary market life insurance policies offer as an investment for doctors?

US secondary market life insurance policies offer three key advantages, especially for doctors, which clearly differentiate them from traditional capital investments:

1. Return Logic Based on Medical Expertise

Economic success is not based on stock market forecasts or market sentiment, but on medical analysis. Before each investment, comprehensive health records are evaluated and supplemented by independent life expectancy assessments. This principle is particularly understandable for doctors, as it involves probabilities, diagnoses, and statistical evidence, not speculation.

The more precise the medical assessment, the more accurately the expected term can be calculated. If an insured person dies earlier than originally projected, this can lead to significantly higher returns than calculated. This creates performance potential from expert analysis.

2. Structurally Very High Payout Security

The crucial point is: Everyone dies. The death benefit is contractually guaranteed. It is not an option, a market value, or an appraisal, but a fixed, defined sum insured.

The policies typically originate from some of the most financially robust and stable insurance companies in the world. These companies have the highest credit ratings and hold enormous capital reserves. Life insurance policies are therefore also used by institutional investors and insurers themselves as sound underlying assets.

The payout does not depend on stock market prices or economic cycles, but on a biological event that is certain to occur. Only the timing remains uncertain.

3. No Classic Risk of Capital Loss, unlike Stocks or Funds

With stocks, funds, or real estate, the market value can permanently fall below the purchase price. With a secondary market policy, however, the contractually stipulated sum insured is paid out in the end.

A negative development is only conceivable in theoretical extreme scenarios, for example, if the insured person lives exceptionally long, significantly beyond their projected life expectancy, thereby requiring additional premium payments. Even in such cases, typically only the return decreases, not automatically the capital invested.

There are no daily price fluctuations or typical downward trends as seen in the stock market. The performance follows a calculable logic.

What are the risks and disadvantages?

As with any investment, US secondary market policies also carry residual risks.

1. Currency Risk (USD/EUR)

Payouts are made in US dollars. If the euro performs unfavorably against the dollar, this can reduce returns in euros. There is only limited influence over this risk, as it depends on global macroeconomic developments.

Assessment: Exchange rates move cyclically. With temporal flexibility, payout times can be strategically chosen, or a portion can be deliberately held as dollar exposure. Nevertheless, currency risk remains the most external influencing factor for this investment.

2. Longevity Risk

If the insured person lives significantly longer than projected, the capital commitment period extends, and additional premiums become due. This reduces the return.

Assessment: This risk is reduced through medical assessments, conservative calculations, and premium buffers. In practice, a longer lifespan typically means a lower return, without resulting in a loss of capital.

3. Complexity and Provider Selection

The market is specialized and legally complex. Lack of experience or inefficient structures can reduce returns.

Assessment: With a specialized partner, policies are carefully reviewed, cost structures are made transparent, and processing is professionally organized.

In summary, the risks are real but structurally calculable. Crucial factors are a careful selection of policies, conservative assumptions, and professional guidance.

How can doctors invest in US secondary market policies?

Basically, there are two ways.

1. Direct Investment in Individual Policies

In direct investment, one or more specific life insurance policies are acquired, usually together with other investors. In practice, this is done through a specialized provider with access to the US market.

A specific amount is invested, covering the policy purchase and premium reserves. The policy is held in trust, for example, through a US trust company or a trust. The investor is the beneficial owner and receives their share of the payout once the policy matures.

Direct investments typically require a minimum investment, often starting from $50,000, as individual policies can cost six-figure dollar amounts and sufficient premium reserves must be factored in. The advantage lies in high transparency, the absence of ongoing fund costs, and clear allocation of the acquired policies.

2. Indirect Investment via Funds or Holdings

Specialized funds or bond models exist that invest in life settlements. These vehicles pool capital from many investors and acquire a larger portfolio of policies.

While smaller amounts can sometimes be invested here, higher costs are often incurred, and terms are fixed. Additionally, there is less influence over which policies are included in the portfolio.

For many doctors who value transparency and having a say, direct investment through a specialized advisor is the preferred option.

In Germany, access to the US secondary market is typically facilitated by specialized financial advisors. They handle structuring, legal details, and the selection of suitable policies.

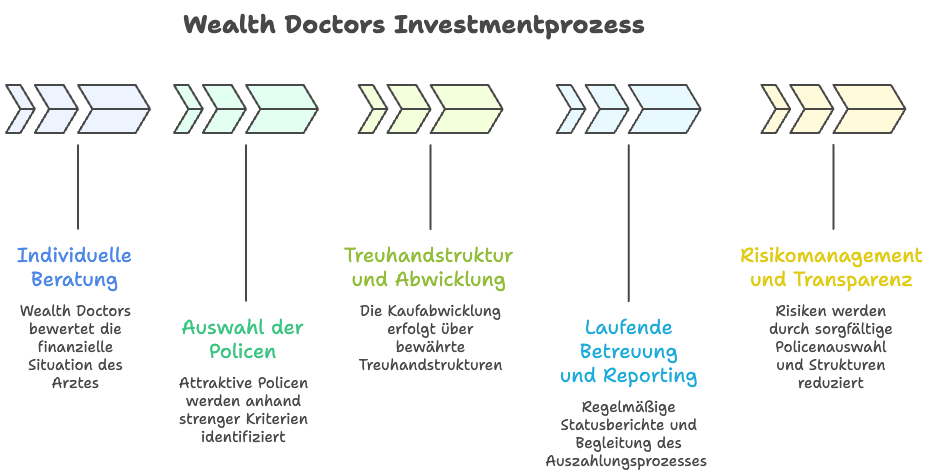

How Wealth Doctors Supports Your Investment

Wealth Doctors provides comprehensive and structured support to doctors for sophisticated investments such as US secondary market policies.

1. Individual Consultation

First, we assess whether life settlements align with your financial goals and individual situation. Investment horizon, liquidity needs, and risk tolerance are analyzed, and all relevant aspects are transparently explained.

2. Policy Selection

Attractive policies are identified based on strict criteria. Only policies from first-class companies with high ratings are selected. Each policy undergoes a double medical review.

Before investing, full transparency is provided regarding the sum insured, health data, determined life expectancy, and the insurer's rating.

3. Trust Structure and Settlement

The purchase process is handled through established trust structures. The invested capital flows into a secured escrow account and from there into the policy purchase.

The policy is placed into a trust or a similar structure. Legal partners ensure a legally sound and clean transaction. The ongoing administration is handled by the trustee company.

4. Ongoing Support and Reporting

Following the investment, regular status reports are provided. Should the insured event occur, the payout process is professionally managed.

Furthermore, there is the option to immediately reinvest disbursed amounts into new policies. If a direct reinvestment occurs without funds flowing to the private level, the tax on the realized gain is generally not triggered initially. This allows for continued utilization of the compound interest effect and strategic expansion of the capital base.

Macroeconomic developments such as exchange rates are continuously monitored.

5. Risk Management and Transparency

Risks are reduced through careful policy selection, dual medical assessments, and financial buffers. Costs and fees are disclosed transparently.

US Secondary Market Policies: The Perfect Investment for Doctors? A Conclusion

In recent years, US secondary market policies have established themselves as a lucrative and crisis-resistant niche investment. For doctors seeking a secure investment, who can commit capital for several years, wish to diversify their assets more broadly, and want to leverage their medical expertise in the valuation logic of an investment, these policies represent a strategically valuable addition to their portfolio.

Whether this investment form is suitable depends on individual circumstances such as investment horizon, liquidity situation, and risk profile.

The key aspects can be summarized as follows.

- Stable Returns Independent of Markets: Life Settlements enable predictable returns in the mid-single to low double-digit percentage range per year, regardless of economic cycles and stock markets. This creates a stable and predictable component in the portfolio.

- Manageable Risk Through Professional Selection:

Risks such as increased longevity of policyholders or currency fluctuations are quantifiable and can be mitigated through diversification, buffers, and structured analysis. - Suitable for investors with a medium to long-term horizon: US secondary market policies are particularly suitable for investors who can commit capital for several years and are looking for a strategic addition outside traditional market cycles.

- De-risking and Diversification: As a largely market-independent source of returns, US life insurance policies complement existing investments such as equity funds, real estate, or private equity, and enhance the structural resilience of the overall portfolio.

US secondary market policies are not a panacea and are not suitable for every investor profile. However, for physicians with available capital and a clear focus on security, predictability, and diversification, they can represent a substantial addition to their asset structure.

Disclaimer: This article is for informational purposes only and does not constitute investment advice in the legal sense. Any investment decision should be tailored to individual circumstances.

- weitere Artikel

.jpeg)

Get to know us personally

At Wealth Doctors, we understand the demanding reality you face: clinic routine, responsibility, and limited time. Our clients particularly value that we speak plainly, not just sell. And that our advice helps them make measurably better decisions. If you want that too, let's talk.