Top tax tips 2026 for doctors: Save smartly and sustainably with investments

In Germany, doctors are among the top earners. However, high income also comes with a correspondingly high tax burden, which often reaches up to 45 percent. Many medical professionals therefore feel that, despite good pay, they retain too little of their own income. But there are ways to reduce this burden. Targeted tax optimization for doctors helps reduce levies and create financial leeway. Those who optimize their investments for tax purposes not only save money with the tax office but also build wealth at the same time.

In this article, we show which strategies are particularly useful for doctors – from retirement provisions and capital market investments to alternative assets. This article focuses exclusively on tax-optimized securities investments and not on real estate or practice-related topics, which are covered in the second part "Saving Taxes with Real Estate & Practice" will be discussed.

Retirement Provision as a Tax-Optimized Investment

Retirement provision is one of the most important levers when it comes to saving taxes. Although doctors pay mandatory contributions to their professional pension scheme, which are tax-deductible, these are not sufficient due to demographic changes to secure their accustomed standard of living in old age. To close this gap, the state offers attractive opportunities to build wealth and save taxes at the same time.

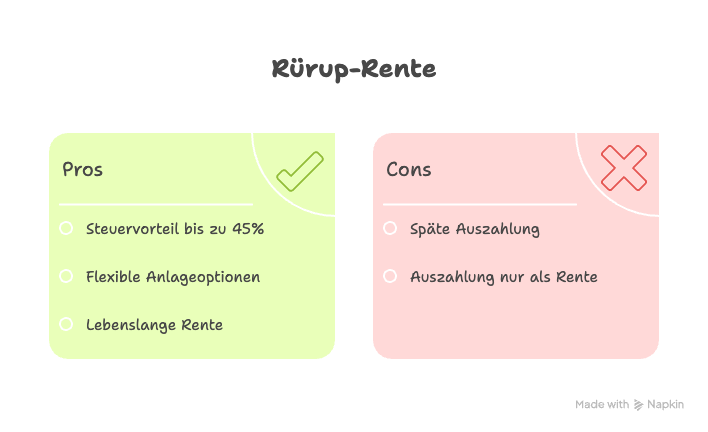

Rürup Pension: An Attractive Foundation for Doctors in the Top Tax Bracket

The Rürup pension, also known as the basic pension, is particularly interesting for doctors who pay the maximum income tax rate. According to § 10 EStG the contributions are considered precautionary expenses, which are tax-deductible up to certain maximum amounts. This significantly reduces the tax burden each year.

The investment form can be freely chosen and adjusted over time.

However, it should be noted that the invested sums can only be paid out as a lifelong pension from the age of 62 at the earliest.

Source: Self-generated with Napkin.ai

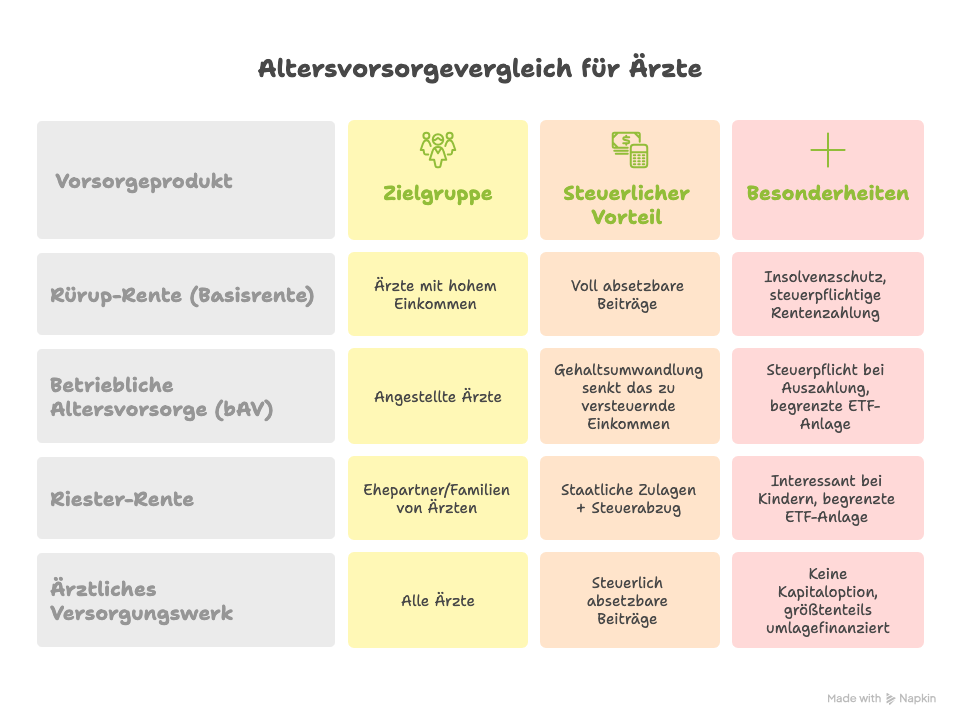

Occupational Pension Scheme: A Benefit for Employed Doctors

For employed doctors, the occupational pension scheme (bAV) is a smart way to save on taxes. A portion of the gross salary is directly channeled into the pension scheme, thereby reducing taxable income. In many clinics, the employer also contributes a subsidy, which further boosts the returns. Over the long term, this builds a solid foundation for personal financial security in retirement. However, the expected returns on the invested capital are significantly lower here than, for example, with a basic pension, as large parts of the investment cannot be placed in ETFs. For a bAV to be worthwhile for doctors, the employer should contribute at least 20% as a subsidy.

Long-term financial planning for doctors does not end with retirement provision and investments. The right insurance coverage also plays a central role, as contributions, coverage gaps, and income risks can directly affect overall financial planning. Particularly important are individually tailored private health insurance for doctors and occupational disability insurance for doctors designed specifically for medical professionals.

Riester Pension: Relevant in Specific Situations

The Riester pension is often only of limited use for doctors, as members of professional pension schemes (Versorgungswerke) are not entitled to a Riester pension. Nevertheless, it can be beneficial through a spouse. State subsidies and the special expense deduction make Riester particularly attractive for families with children. However, similar restrictions on investment options apply here as with the occupational pension scheme.

Table 1: Comparison of Pension Products for Doctors

Source: Self-generated with Napkin.ai

Case Study: How a Doctor Saves Taxes with the Rürup Pension

Dr. Müller, a self-employed internist, earns an annual income of €150,000. He decides to contribute €20,000 to the Rürup pension. Since the contributions are § 10 EStG fully tax-deductible, his taxable income is reduced accordingly.

With a tax rate of approximately 42 % , Dr. Müller thus saves around €8,400 in taxes. This means that effectively, the contribution only costs him €11,600, while the full €20,000 is invested in his pension. This transforms a seemingly high tax burden into a strategic investment in the future.

Make Smart Use of Capital Market Investments

ETFs, funds, and stocks promise solid long-term returns and are therefore an important component of balanced wealth accumulation. Investment income in Germany is generally subject to capital gains tax. The capital gains tax on profits from stocks, funds, or interest in Germany is 26-28% (including solidarity surcharge and church tax, where applicable).

With the right strategies, doctors can significantly reduce their tax burden and retain more capital in their portfolios.

Maximize the saver's allowance

The first step to tax optimization in the capital market is to utilize the saver's allowance. Single individuals can keep up to 1,000 Euros in investment income tax-free, while for married couples, the allowance is 2,000 Euros per year. Anyone who submits a tax exemption order to their bank ensures that these amounts are not unnecessarily taxed. This simple but effective step is particularly worthwhile for doctors who regularly invest in ETFs or funds.

Important to know: Children also have their own saver's allowance. Therefore, savings plans should ideally be in the child's name – this way, the children's tax-free allowances are optimally utilized.

Utilize the tax advantages of funds

Another important point is the partial exemption for funds. For equity funds, 30 percent of the income is tax-free, and for real estate funds, it's up to 80 percent. This tax benefit makes funds even more attractive compared to individual stocks, as it boosts the net return. Therefore, those investing long-term should also consider the tax treatment when selecting funds.

Buy-and-Hold and Accumulation as a Tax Advantage

A long-term investment strategy offers doctors additional advantages. Profits from stocks and funds are only taxed upon sale. Therefore, those who invest according to the "Buy-and-Hold" principle defer the tax burden into the future and benefit from the compound interest effect in the meantime. Accumulating funds, which automatically reinvest their earnings, are particularly interesting. This allows the invested capital to grow continuously without annual taxes on distributions.

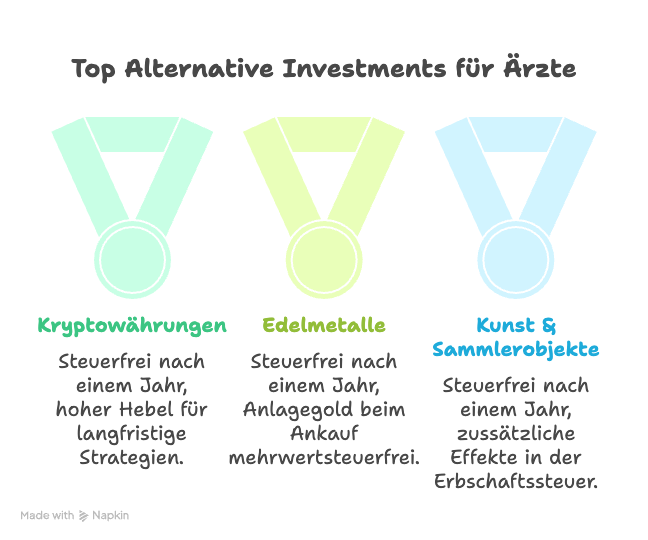

Alternative Investments for Greater Diversification

In addition to traditional investments, alternative investments can also play an exciting role in wealth planning. They offer doctors the opportunity to broaden their portfolio and utilize tax advantages. Cryptocurrencies, precious metals, and art are particularly interesting in this regard.

According to § 23 EStG gains from private disposals are tax-free if the holding period is at least one year. This applies to cryptocurrencies, precious metals, and works of art.

Cryptocurrencies: Tax-free after one year

Cryptocurrencies like Bitcoin or Ethereum have received a lot of attention in recent years. For investors, they are interesting not only because of their high price volatility but also due to their tax treatment. Anyone who holds their coins for at least one year can realize profits from their sale completely tax-free. For short-term sales, the saver's allowance of up to 1,000 Euros per year applies, provided it has not already been used for gains from other investments.

Precious Metals as Stable Tangible Assets

Precious metals like gold or silver are also a proven means of securing assets. Gold has the additional advantage that there is no VAT on the purchase of investment gold. If the precious metal is held for more than one year, capital gains are also tax-free. This applies only to precious metals that are physically held, not to certificates or similar.

For doctors who wish to conservatively secure a portion of their assets, precious metals are a solid addition to their portfolio.

Art and Collectibles as a Tax Niche

Another area includes artworks, classic cars, or other collectibles. Here too, if they are held for more than one year, profits from a sale are tax-free. In certain cases, this also presents interesting opportunities for inheritance tax planning.

For doctors with a passion for art or classic vehicles, this can be not only a hobby but also a clever tax strategy.

Conclusion: Saving Taxes is Legal and Sensible

Doctors have numerous opportunities to reduce their tax burden while simultaneously building wealth. Whether through a Rürup pension, capital market investments, or alternative assets, the options are vast. The key is to find the right combination that suits one's personal situation. With professional support, all tax advantages can be maximized, ensuring more income remains at the end.

Thus, a seemingly high tax burden transforms into a real opportunity: fewer payments to the state, more financial flexibility, and long-term security.

This article is Part 1. In Part 2, we will show how doctors can utilize further significant tax levers with real estate and practice investments.

- weitere Artikel

Get to know us personally

At Wealth Doctors, we understand the demanding reality you face: clinic routine, responsibility, and limited time. Our clients particularly value that we speak plainly, not just sell. And that our advice helps them make measurably better decisions. If you want that too, let's talk.